Table of Contents

If you run a business in the UK, the VAT rate on your electricity bill is almost certainly costing you more than it should. Most businesses pay 20% VAT on electricity without ever checking whether they qualify for the reduced 5% rate. HMRC will not come knocking to tell you that you are overpaying. That responsibility sits entirely with you and depends on whether your energy supplier is billing you correctly in the first place.

This guide covers exactly which VAT rate applies to your business electricity bill, who qualifies for 5%, how to claim it, and what else drops off your bill when the rate changes. Because VAT is only part of the overall saving.

Quick Answer: What Is the VAT Rate on Business Electricity?

The standard VAT rate on business electricity is 20%. That is what HMRC applies to commercial energy supplies by default and what your supplier will charge unless you actively qualify for something different.

The reduced rate of 5% is available to businesses meeting specific criteria under HMRC VAT Notice 701/19. These include low-usage businesses below the de minimis threshold, charities using energy for non-business activities, and mixed-use premises where at least 60% of electricity is used for qualifying domestic or charitable purposes.

How VAT on Business Electricity Actually Works

HMRC classifies electricity as “fuel and power” and applies its own rules to determine the correct rate. The default for any commercial supply is 20%. To access the 5% rate, the supply has to fall into one of HMRC’s qualifying categories, and in most cases the business has to inform their supplier. Suppliers rarely volunteer this information proactively.

One thing many businesses completely miss: VAT applies to your entire bill, not just the unit rate for electricity consumed. Standing charges, supply charges, and any inseparable costs on the same bill are all taxed at the same rate as the electricity itself. If your electricity qualifies for 5%, your standing charge does too. If you have been charged 20% when you should have been on 5%, the overpayment covers every line on every bill.

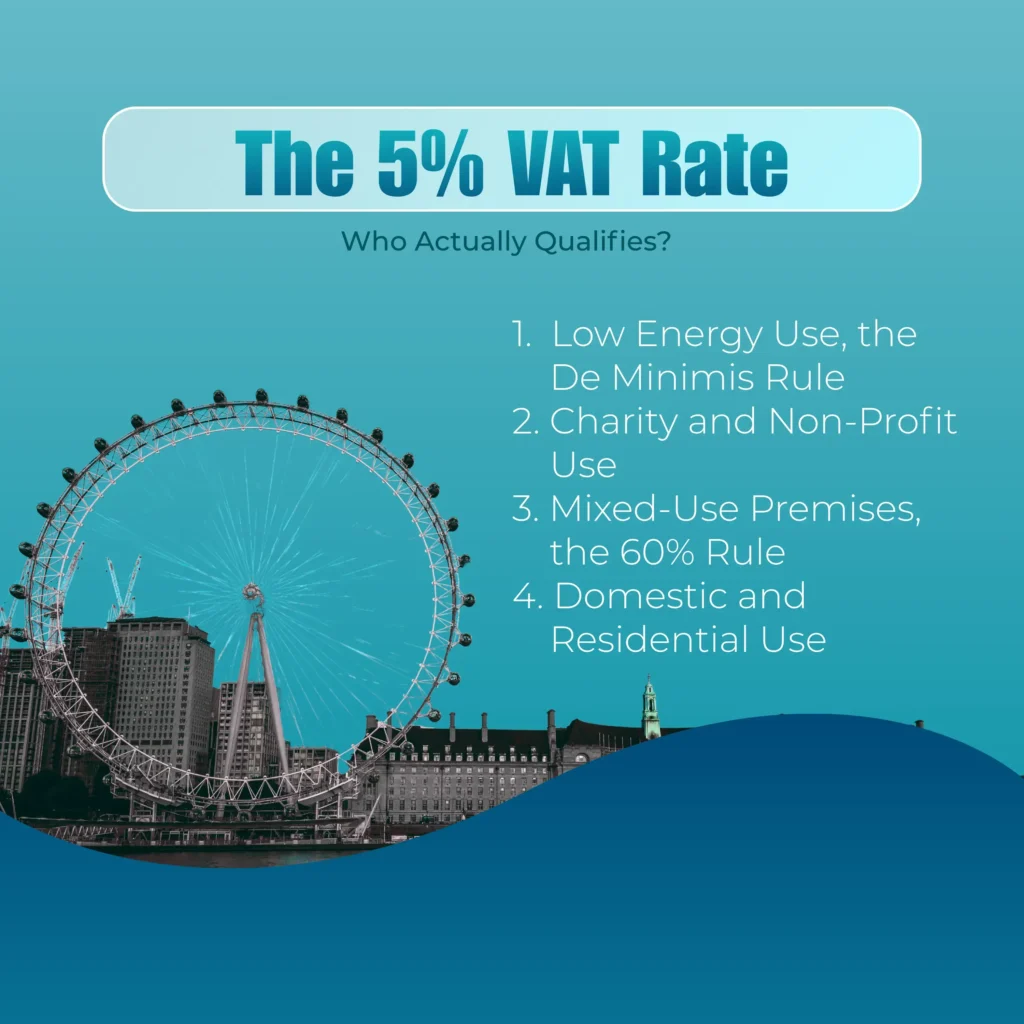

The 5% VAT Rate: Who Actually Qualifies?

1. Low Energy Use, the De Minimis Rule

This is the most commonly missed qualification and the one most relevant to small businesses. If your business uses no more than an average of 33 kWh of electricity per day or 1,000 kWh per month, HMRC treats the entire supply as domestic in nature. The rate drops to 5% regardless of what your business actually does.

You do not need to be a charity. You do not need domestic accommodation on site. You just need to be below the threshold.

To put that into practical terms: a small office running computers, lighting, and basic appliances will typically use between 300 and 800 kWh per month. Many of those businesses are sitting below 1,000 kWh right now, paying 20% VAT, and have no idea they qualify for 5%.

Pull out your last three electricity bills and check the monthly kWh figure. If it is consistently under 1,000 kWh, there is a strong chance you are on the wrong rate.

2. Charity and Non-Profit Use

Registered charities can qualify for 5% when electricity is used for non-business activities. HMRC is specific here: the energy must power the charitable activity itself, such as free care, community services, or residential accommodation, rather than any trading arm such as a charity shop or café.

Charities with mixed activities need to be careful. Where the majority of energy use is for qualifying non-business charitable activity, the reduced rate can apply. Where there is a genuine mix, a VAT declaration and sometimes an apportionment calculation will be needed before the supplier can make the change.

3. Mixed-Use Premises, the 60% Rule

Where premises are used for both commercial and qualifying domestic or charitable purposes, HMRC applies a 60% rule. If 60% or more of the electricity supply is for qualifying use, the whole supply can be charged at 5%. Below 60%, the bill must be apportioned, part at 5% and part at 20%.

This applies to more situations than most businesses realise:

- A pub or restaurant with living accommodation above

- A care home with some commercial services

- A business operating from a property that also contains a flat

- A farm with domestic and agricultural electricity on the same meter

- A religious building with residential accommodation attached

In each case, the supplier will need a VAT declaration form and evidence of the usage split before they can apply the reduced rate.

4. Domestic and Residential Use

Electricity supplied to properties used purely as domestic accommodation, including student accommodation, care homes, self-catering holiday lets, hospices, and children’s homes, qualifies for 5%. This matters for landlords and property managers who supply electricity to tenants and need to understand the correct VAT treatment on their own energy accounts.

The Hidden Saving: VAT and the Climate Change Levy

This is the angle most guides skip entirely, and it is worth real money.

If your business qualifies for the 5% VAT rate under the de minimis rule, HMRC also exempts your supply from the Climate Change Levy (CCL). These two reliefs are directly linked. Qualify for one and you automatically qualify for both.

The CCL is a government environmental tax charged on business energy. From 1 April 2026, the rate is 0.801 pence per kWh on both electricity and gas, rising further from April 2027. It appears as a separate line on your bill, and most businesses simply pay it without question.

For a small business using 900 kWh of electricity per month, the CCL charge adds up to roughly £86 per year on top of VAT. That is money leaving your business every year purely because nobody flagged the exemption.

When you submit a VAT declaration form to your supplier confirming you qualify under the de minimis rule, the supplier removes both the 20% VAT rate and the CCL charge in one step. You do not need separate forms. The combined saving makes this the single most valuable billing correction most small businesses can make.

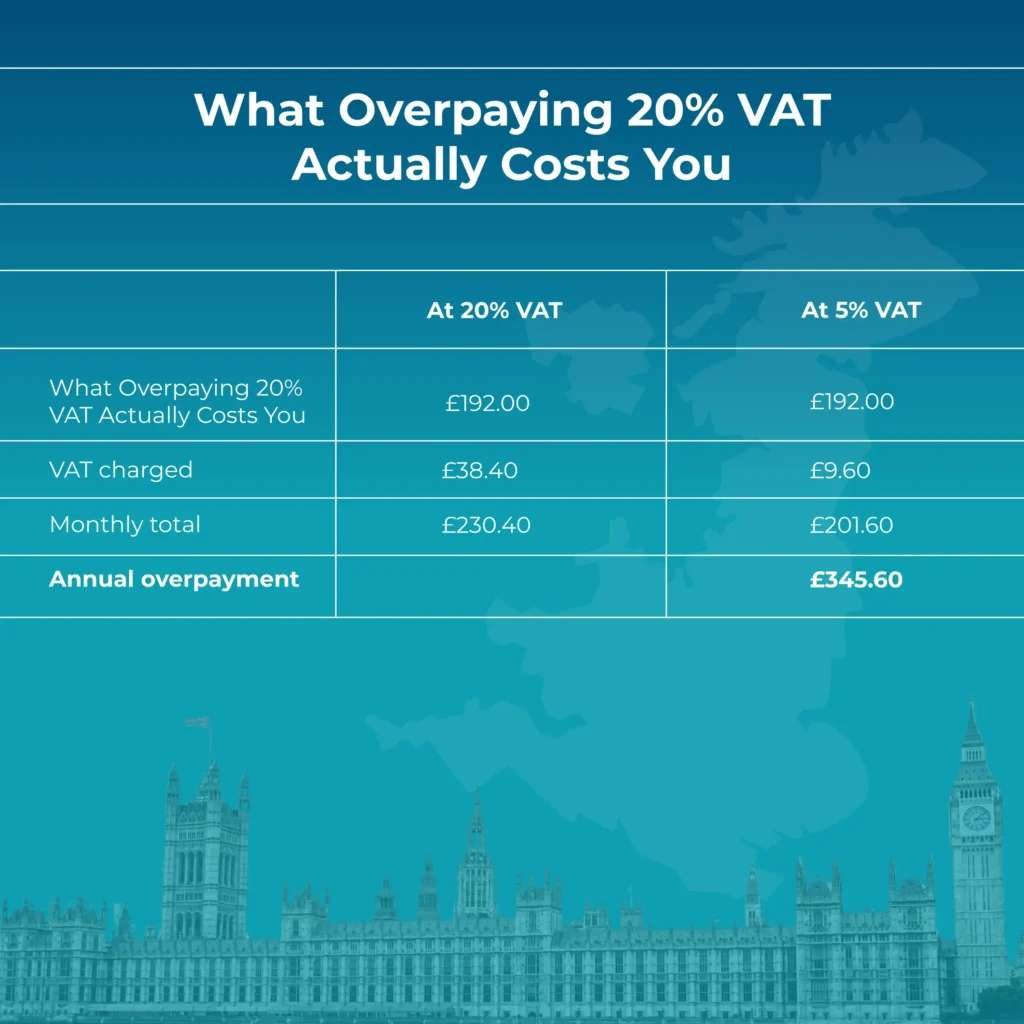

What Overpaying 20% VAT Actually Costs You

Here is a worked example with real numbers.

A small retail unit uses 800 kWh of electricity per month, comfortably below the 1,000 kWh de minimis threshold. Their supplier charges 24p per unit, excluding VAT and standing charges.

| Bill Breakdown | At 20% VAT | At 5% VAT |

| Monthly electricity cost (ex-VAT) | £192.00 | £192.00 |

| VAT charged | £38.40 | £9.60 |

| Monthly total | £230.40 | £201.60 |

| Annual overpayment | £345.60 |

Add the CCL exemption saving of roughly £77 per year, and the total annual saving from correcting the billing reaches around £420 per year. For a business that simply never submitted a VAT declaration form.

If the business has been on the wrong rate for three years, that is approximately £1,260 that can be reclaimed. At four years, around £1,680. All for the cost of one phone call.

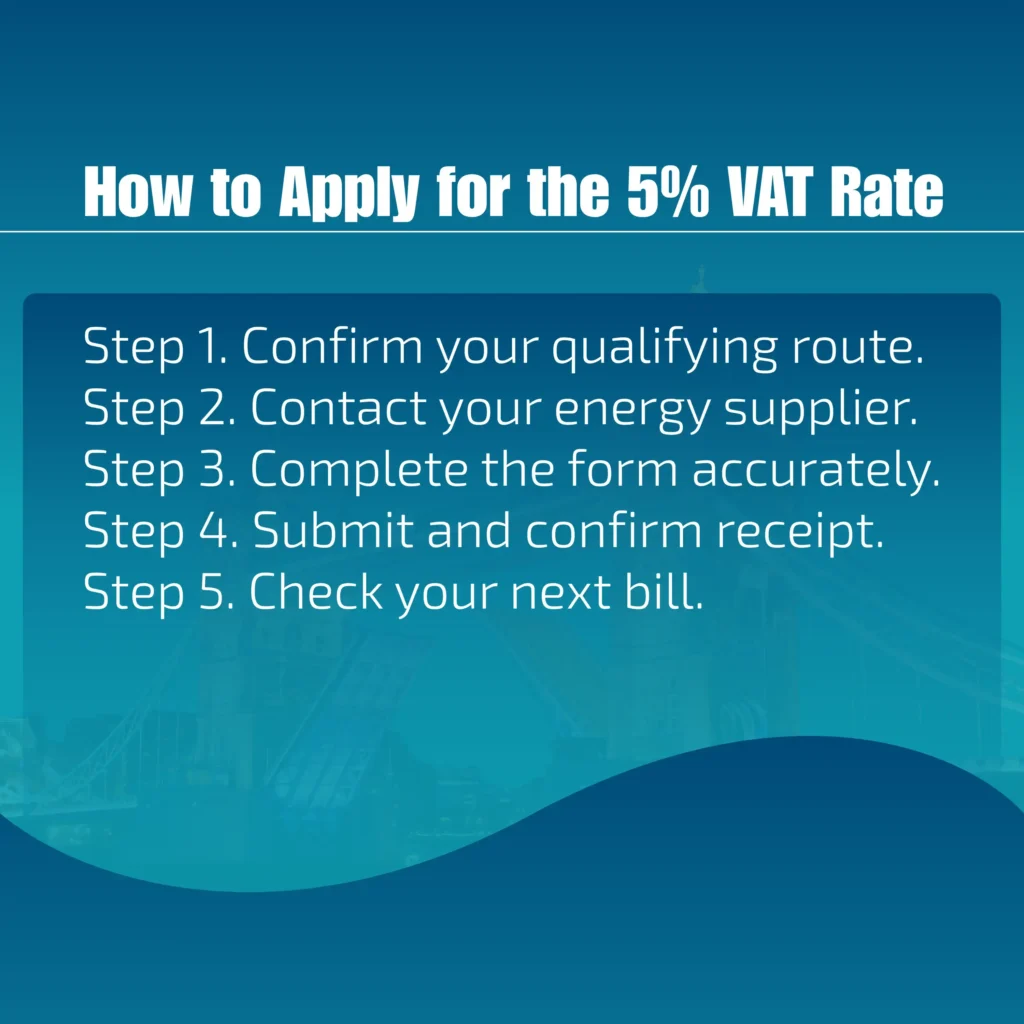

How to Apply for the 5% VAT Rate

Step 1. Confirm your qualifying route. Check your monthly kWh usage on your last three bills. If you are consistently under 1,000 kWh per month, you qualify under the de minimis rule. If your site has mixed use or charity activity, work out the percentage of qualifying use before contacting your supplier.

Step 2. Contact your energy supplier. Call the business customer line and ask for a VAT declaration form. Every major supplier has one. Search for “[your supplier name] VAT declaration form” or ask the customer service team to email it directly. British Gas Business, EDF, E.ON, Octopus, and SEFE all have their own versions.

Step 3. Complete the form accurately. The form will ask which qualifying route applies, your meter reference number, and a calculation or statement confirming your qualifying status. Keep a copy for your records.

Step 4. Submit and confirm receipt. Send by email and ask for written confirmation of receipt and when the rate change takes effect. British Gas Business, for example, aims to process declarations within 28 days and applies the reduced rate from the date the valid certificate is received.

Step 5. Check your next bill. Confirm that the VAT line now shows 5% and that CCL has been removed where applicable. If nothing has changed, contact the supplier with your submission confirmation and escalate if needed.

Can You Reclaim Overpaid VAT on Past Electricity Bills?

Yes, and this is the part most businesses never act on.

HMRC allows backdated corrections going back up to four years from the date the error is discovered. If your supplier has been charging 20% when you should have been on 5%, you can submit a backdated VAT declaration and request a correction covering all bills within that four-year window.

The process:

- Submit your VAT declaration with a backdated effective date, the date your qualifying use began, up to four years ago.

- Ask the supplier explicitly for a bill correction and credit note covering the overpaid amount.

- If the supplier resists or delays beyond eight weeks, raise a formal complaint. If still unresolved, escalate to the Energy Ombudsman, who can make binding decisions on billing disputes.

- For significant overpayments above £10,000, or where the supplier is uncooperative, you may need to report a VAT error correction directly to HMRC. An accountant can advise on the right route here.

Put everything in writing at every stage. A paper trail makes disputes considerably easier to resolve.

Special Situations: VAT by Business Type

Working from Home

If you run your business from home, HMRC says you pay 5% on the domestic portion of your electricity and 20% on the business portion. In practice, most home-based businesses use a domestic energy account for the whole property, and the rate is 5% across the board unless commercial activity pushes total usage above 1,000 kWh per month. If you run a larger home-based operation, a workshop, salon, or studio, it is worth checking whether your monthly usage has crossed that threshold.

Businesses with Multiple Meters or Sites

Each electricity meter has its own VAT status. A business with six sites cannot submit one declaration for all of them. Each account must be assessed independently. Opening a new site, relocating, or reclassifying use at an existing site resets the VAT assessment for that meter. If you manage multiple premises, review each one separately.

Landlords Supplying Electricity to Tenants

Landlords who supply electricity to tenants through a sub-meter or communal system need to understand the VAT treatment of their own supply account. If the property is residential and the electricity is used domestically, the 5% rate should apply to the landlord’s account even if they are a commercial operator.

Businesses Close to the Threshold

If your monthly usage fluctuates around 1,000 kWh, your VAT rate can technically shift month to month. In practice, HMRC bases the de minimis assessment on average daily use, and suppliers typically apply a consistent rate based on a review of recent meter readings. Keep an eye on usage after any significant changes to equipment, premises, or operating hours.

How to Check the VAT Rate on Your Bill Right Now

Open your most recent electricity bill and look for:

- A line showing VAT at 20% or VAT at 5%, clearly itemised

- A separate line for Climate Change Levy or CCL, shown in pence per kWh

- Your monthly kWh consumption figure, compared against the 1,000 kWh threshold

If your bill shows 20% VAT and your monthly consumption is below 1,000 kWh, you are almost certainly on the wrong rate. If it shows CCL charges and your usage is below the threshold, that charge should disappear once you submit the declaration.

If VAT is not clearly broken out on your bill, ask your supplier for a fully itemised VAT invoice. HMRC requires suppliers to show VAT information clearly on business invoices.

VAT on Business Electricity vs Business Gas: Is There a Difference?

The qualifying rules are the same for both, but the de minimis thresholds differ. For gas, the reduced rate applies where usage falls below 145 kWh per day or 4,397 kWh per month. Gas is typically consumed at much higher volumes than electricity, so fewer businesses fall under this threshold, but heating-only sites, small units, or businesses with minimal gas use may still qualify.

If you have both an electricity account and a gas account, assess each one separately under its own threshold. It is entirely possible to qualify for 5% on electricity but not on gas, or the other way around.

Frequently Asked Questions

What is the VAT rate on business electricity in the UK?

The standard rate is 20%. The reduced rate of 5% applies to qualifying supplies under HMRC VAT Notice 701/19, including businesses using under 1,000 kWh per month, charities using energy for non-business activities, and mixed-use premises where at least 60% of use qualifies.

Is electricity VAT 5% or 20% for businesses?

It depends on your usage and premises type. Most businesses default to 20%. Low-usage businesses, charities, and mixed-use sites can access 5%.

Does VAT apply to the standing charge on my electricity bill?

Yes. Where the bill includes electricity and inseparable standing or supply charges, the whole bill is taxed at the same VAT rate as the electricity itself.

Do I need to apply for the 5% rate or is it automatic?

For most qualifying businesses, you need to submit a VAT declaration form to your supplier. Some low-usage sites are automatically billed at 5% if metering data confirms usage below the threshold, but many suppliers default to 20% and wait for a declaration. Do not assume it is being applied correctly. Check the bill.

Can I reclaim overpaid VAT on old electricity bills?

Yes. HMRC allows backdated corrections up to four years. Submit a backdated VAT declaration to your supplier and request a credit note for the overpaid amount.

What is the CCL and does it relate to VAT?

The Climate Change Levy is a separate government tax on business energy, currently 0.801p per kWh from April 2026. If you qualify for 5% VAT under the de minimis rule, you are also exempt from CCL on the same supply. Both reliefs are applied via the same VAT declaration form.

Does working from home mean I pay 5% or 20% VAT on electricity?

If your domestic energy account covers the whole property, the rate is 5% as standard. If your usage crosses 1,000 kWh per month due to business activity, the commercial portion may be treated differently.

Do business rates include VAT?

Business rates, the local property tax on commercial premises, are completely separate from VAT. They do not include VAT and are not charged through your energy bill.

Check Your Bill, Not Your Assumptions

The VAT rate on business electricity is 20% by default, but a significant number of UK businesses should be paying 5% and are not. The 1,000 kWh per month de minimis threshold catches more businesses than most people expect. Charities, mixed-use premises, and home-based businesses have additional routes to the reduced rate.

Correcting the rate does not just reduce VAT. It removes the Climate Change Levy too. And if the wrong rate has been applied for years, a backdated reclaim covering up to four years is available.

The single most useful thing you can do right now is check your monthly kWh figure on your last electricity bill. If it is under 1,000 kWh, call your supplier today and ask for a VAT declaration form.

If you want someone to review your current energy contracts and VAT treatment as part of a wider cost comparison, an energy broker can review your contracts, check your VAT treatment, and ensure your next agreement is structured correctly from day one.